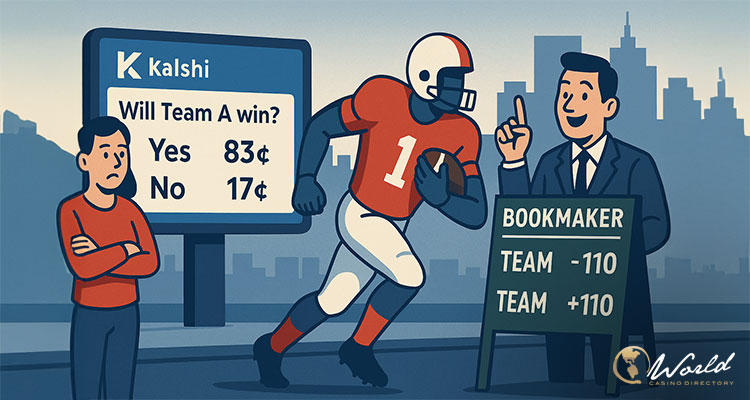

During the opening week of the NFL season, prediction market operator Kalshi came under pressure after analysts determined its betting prices were consistently less competitive than those at major sportsbooks. A study by Citizens JMP Securities, cited by Next.i,o revealed that bettors using Kalshi faced higher effective costs for both moneyline and over/under wagers compared to DraftKings and FanDuel once transaction fees were factored in.

The research challenged a widespread belief among bettors and industry observers: that exchanges naturally deliver sharper odds than traditional sportsbooks. “Despite some in the industry pushing the notion exchanges have better pricing, this is currently not true for the average consumer according to the data we tracked during Week 1 of the NFL season,” analysts stated.

Fees Create Pricing Disadvantage

At the heart of Kalshi’s weaker pricing is its fee structure. Unlike sportsbooks that build their profit margin into the vig, Kalshi applies transaction fees to each trade. Citizens’ review showed retail customers typically pay about $1.63 for every 100 moneyline contracts and $1.75 for equivalent over/under positions. While the platform extends more favorable conditions to institutional players and market makers, retail users end up absorbing higher effective costs.

According to Citizens analyst Jordan Bender, that structure erased any perceived edge. Bender’s tracking of pregame lines on September 5 demonstrated that Kalshi’s moneyline and total wagers were 10% and 25% more expensive than DraftKings, and 16% and 23% higher than FanDuel, respectively. By kickoff on Sunday, pricing had narrowed but remained worse — about 7% more costly on moneylines and 10% on totals across both leading sportsbooks.

Growth in Trading Volume, But Questions Remain

The scrutiny over pricing came just as Kalshi was celebrating record activity from college football. The platform processed $84.9 million in trades during the first full Saturday of the NCAA season, with nearly $59.8 million tied specifically to college football contests. That activity generated $914,000 in fee revenue — nearly a million-dollar day, the highest for Kalshi outside of the 2024 U.S. election.

Expectations were even higher heading into NFL Week 1. In the week prior, Kalshi recorded roughly $1.6 million in trades on upcoming Sunday NFL matchups, almost double the advance activity seen before college football’s opening weekend. Analysts suggested this surge could translate to trading volumes of $150–200 million on pro football contracts alone, with total daily volume potentially pushing close to $250 million when other events were included.

Because Kalshi earns around one cent per dollar traded, NFL Week 1 had the potential to generate between $1.5 million and $2 million in fees. The exact figure depends on how evenly matched games were, since closer odds produce higher effective fees per dollar.

Parlays and Cash-Outs: More Limitations Ahead?

Beyond pregame odds, Kalshi’s product set is also under the microscope. The company recently filed to introduce multi-legged contracts that would serve as its version of parlays, a category that has become a profit engine for traditional operators like DraftKings and FanDuel parent Flutter Entertainment. However, analysts caution that these products may also prove less attractive to bettors. “We expect pricing to be even more inferior compared to DraftKings and FanDuel with the collateral needed by the market makers to trade the product,” Bender warned.

Kalshi’s cash-out feature has likewise drawn skepticism. Although the exchange promotes the option as an advantage over sportsbooks, analysts argue its real-world utility is limited because Kalshi does not yet support parlays, where early settlement is most valuable.

Competitive Threat Still Limited

Despite Kalshi’s growing trading volume and product expansion, many in the industry remain unconvinced that the platform poses an immediate risk to sportsbooks. Bender summarized the view: “Together with inferior pre-game pricing, UI/UX, and cashout, we do not view betting exchanges as a competitive threat to profitability for existing operators (DKNG, FLUT, MGM Resorts Caesars Entertainment, PENN Entertainment, Rush Street Interactive) in the legal sports betting states and should not expect to see reactionary promos/marketing as a result.”

Even with rivals such as Crypto.com, Robinhood, and Polymarket preparing their own offerings, Citizens’ analysis suggests the edge still lies with established sportsbook operators. For now, prediction markets like Kalshi may drive volume, but bettors looking for value are likely to continue favoring sportsbooks like DraftKings and FanDuel.